-3.png?width=50&name=Square%20(2)-3.png)

TLDR; we cover, Why Premiums Increased How Does the SGD4.1 Billion Government Aid Help? Key...

The MediShield Life Council's recommendations come in response to the evolving landscape of healthcare needs and expenses. The key considerations behind these recommendations include the need to address the following critical aspects:

- Coverage Erosion: Rising medical costs have diminished the coverage provided by the existing claim limits, resulting in MediShield Life fully covering just under eight in ten subsidised bills in public healthcare institutions.

- Shifting Healthcare Dynamics: There has been a notable transition in healthcare delivery from hospitals to outpatient, community, and home settings, areas that MediShield Life currently does not comprehensively cover.

- Advancements in Medical Technologies: The emergence of new and potentially life-saving therapies, such as Cell, Tissue, and Gene Therapy Products (CTGTPs), poses a challenge as these are not within the current coverage scope of MediShield Life.

Enhancements to Benefits and Scheme Parameters

To address these challenges and provide better coverage to policyholders, the following enhancements have been proposed:

Image source: Ministry of Healeth Singapore: Government Accepts Medisave Council's Recommendations

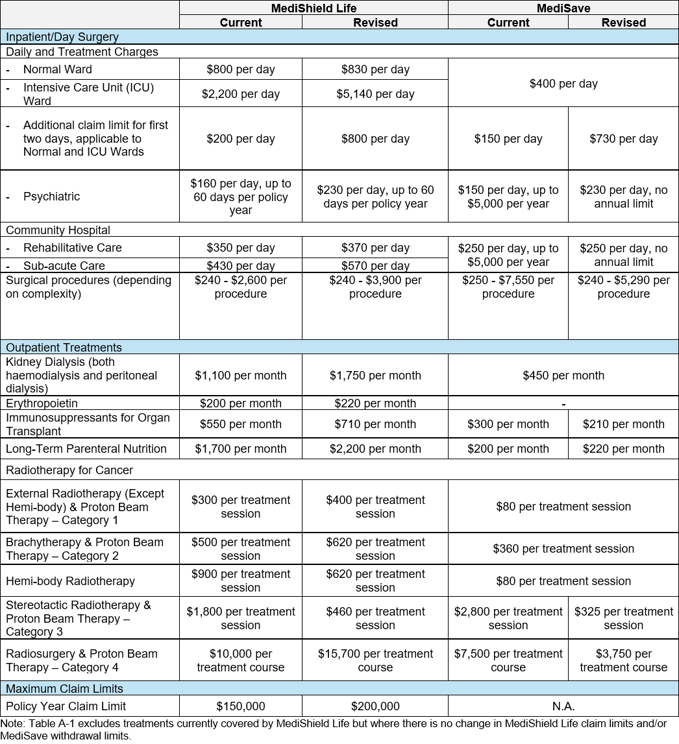

Inpatient and Day Surgery Coverage

- Increased Claim Limits: The claim limits for inpatient and day surgery expenses will be raised to fully cover nine in ten subsidised bills, offering greater financial protection.

- Policy Year Claim Limit: To provide additional assurance, the policy year claim limit will be elevated from $150,000 to $200,000.

- Inpatient Deductible Adjustment: An increase in the inpatient deductible will be implemented, focusing coverage on larger bills and helping moderate premium increments.

- Revision of Pro-ration Factors: Private unsubsidised bills' pro-ration factors will be revised to prevent cross-subsidisation, ensuring fair billing practices.

Outpatient Coverage Expansion

- Enhanced Claim Limits: Outpatient claim limits will be refreshed to cover a higher percentage of subsidised bills, including new treatments and home-based medical care.

- Outpatient Deductible Introduction: A new outpatient deductible of $500 per year will be introduced to manage larger bills effectively.

- Co-insurance Adjustment: Co-insurance for outpatient treatments will transition from a flat 10% to a tiered structure, making larger outpatient bills more affordable.

Coverage Extension to High-Cost Treatments

- Clinical and Cost-effective Treatments: The scheme will now encompass high-cost treatments that have proven clinical effectiveness and cost-efficiency, ensuring improved access and affordability.

Premium Adjustments and Government Support

As a result of the enhancements and expanded coverage, premiums will see adjustments. To mitigate the impact on policyholders, the following measures will be undertaken:

- Premium Increase Cap: Premium increases will be capped at 35% and phased in evenly over three years, starting from April 2025.

- Government Support: The Government will provide additional support measures, including MediSave top-ups and premium subsidies, amounting to $4.1 billion over the next three years to offset premium hikes for the majority of Singaporeans.

Government's Approval and Implementation Timeline

The Singaporean Government has endorsed the recommendations, ensuring that MediShield Life continues to offer meaningful protection to its citizens. The revised benefits and adjusted MediSave withdrawal limits will be gradually implemented starting from April 2025.

In conclusion, these enhancements to the MediShield Life scheme signify a proactive approach to addressing the evolving healthcare landscape, ensuring that Singaporeans receive comprehensive coverage and financial support when facing significant health challenges.

Household Archetypes and Worked Examples

Here are some practical examples to understand how these mechanisms work for individuals and families in need.

-

-

Mr A - The Independent Senior

- Mr A is a single Merdeka Generation senior at 67 years old, residing in a 2-room HDB flat with a modest per capita household income of $1,000 monthly. Despite his limited financial resources, Mr A is entitled to means-tested subsidies of 40%, along with additional MG subsidies of 5%. Furthermore, he receives support to phase in any premium increase evenly over the next three years.

Note: Figures in brackets refer to the increase in premiums using 2024 as the base year. Cumulative increase over 2025 to 2027 refers to the sum of the figures in brackets.

Image source: Ministry of Healeth Singapore: Government Accepts Medisave Council's Recommendations

- Mr A is a single Merdeka Generation senior at 67 years old, residing in a 2-room HDB flat with a modest per capita household income of $1,000 monthly. Despite his limited financial resources, Mr A is entitled to means-tested subsidies of 40%, along with additional MG subsidies of 5%. Furthermore, he receives support to phase in any premium increase evenly over the next three years.

-

-

-

Mrs B - The Elderly Beneficiary

- Mrs B is a single Pioneer Generation senior aged 87, living in a 2-room HDB flat with no household income. Despite her financial constraints, Mrs B benefits from special PG subsidies of 59% and an annual PG MediSave top-up of $700. Similar to Mr A, she also receives support to phase in any premium increase over the next three years.

Note: Figures in brackets refer to the increase in premiums using 2024 as the base year. Cumulative increase over 2025 to 2027 refers to the sum of the figures in brackets.

Image source: Ministry of Healeth Singapore: Government Accepts Medisave Council's Recommendations

- Mrs B is a single Pioneer Generation senior aged 87, living in a 2-room HDB flat with no household income. Despite her financial constraints, Mrs B benefits from special PG subsidies of 59% and an annual PG MediSave top-up of $700. Similar to Mr A, she also receives support to phase in any premium increase over the next three years.

-

Mr and Mrs C - The Affluent Couple

- Mr and Mrs C, are a Merdeka Generation senior couple aged 67, residing in a private residential property with a per capita household income exceeding $3,600. Despite their relatively comfortable financial situation, they still benefit from MG subsidies of 5% and support to phase in any premium increase evenly over the next three years.

Note: Figures in brackets refer to the increase in premiums using 2024 as the base year. Cumulative increase over 2025 to 2027 refers to the sum of the figures in brackets.

Image source: Ministry of Healeth Singapore: Government Accepts Medisave Council's Recommendations

- Mr and Mrs C, are a Merdeka Generation senior couple aged 67, residing in a private residential property with a per capita household income exceeding $3,600. Despite their relatively comfortable financial situation, they still benefit from MG subsidies of 5% and support to phase in any premium increase evenly over the next three years.

-

The D Family - A Multigenerational Unit

- D family, comprising a grandfather and grandmother, both 67-year-old MGs, a working husband and wife aged 42, and their primary school-going daughter and son. This multigenerational family resides in a 5-room HDB flat with a per capita household income of $2,500 monthly.

The D family benefits from means-tested subsidies of up to 35%, additional MG subsidies of 5%, and support to phase in any premium increase over three years. After considering subsidies and phasing, their cumulative net premium increase of $722 is fully offset by the enhanced MediSave Bonus of $3,500. This bonus is distributed among the grandparents and parents, with additional support from the MediSave Grant for Newborns for the children.

Note: Figures in brackets refer to the increase in premiums using 2024 as the base year. Cumulative increase over 2025 to 2027 refers to the sum of the figures in brackets.

Image source: Ministry of Healeth Singapore: Government Accepts Medisave Council's Recommendations

- D family, comprising a grandfather and grandmother, both 67-year-old MGs, a working husband and wife aged 42, and their primary school-going daughter and son. This multigenerational family resides in a 5-room HDB flat with a per capita household income of $2,500 monthly.

-

You can now be our community contributor and make a pitch to have your favourite personality be on our show.

Join our community group and drop us your insights on this topic.